Figuring out what a home really costs goes way beyond the sticker price. It's a messy calculation that pulls in everything from the purchase price and interest rates to property taxes and your own personal income.

It’s a lot like the true cost of owning a car. You don't just pay the price on the window; you're also on the hook for gas, insurance, and all the maintenance that comes with it. Housing works the same way.

Decoding the High Cost of Housing

Trying to make sense of the housing market today can feel like an uphill battle, whether you're looking to rent, buy, or invest. Prices often feel completely detached from what the average person earns, turning affordability into a major headache for millions.

This isn't just a local problem, either. It’s a global trend where the demand for homes keeps sprinting ahead of the available supply.

The reasons for these eye-watering costs are a mix of big-picture economic forces and local market quirks that have cooked up a tough environment. Getting a handle on these key drivers is the first real step toward making smarter financial moves.

Key Factors at Play

A few powerful forces are driving the affordability crisis. While the exact blend changes from city to city, these three culprits almost always show up at the scene of the crime:

- Persistent Supply Shortages: For decades, we simply haven't built enough new homes to keep up with a growing population. This has created a massive, fundamental imbalance.

- Economic Policies and Interest Rates: Big decisions on monetary policy, especially around interest rates, directly impact how much it costs to borrow money, which in turn fuels or cools buyer demand.

- Shifting Demographics: With an aging population and more people living in smaller households, we need more individual housing units just to shelter the same number of people.

The underlying problem is that many desirable areas are relatively wealthy and have underbuilt housing for decades. As a result, high-income households bid up the available housing, both purchase prices and rents, while others must pay the premium or move somewhere cheaper.

Now, let's break down each of these factors to see how they connect, how they shape the modern cost of a home, and what it all means for your financial future.

The Global Squeeze on Housing Supply

At the core of sky-high housing costs is a simple economic rule we all know: supply and demand. When more people want something than is actually available, prices shoot up. We see it with concert tickets and gas prices, and the same thing is happening with housing not just locally, but on a global scale. It's creating a serious affordability crisis.

Picture a city where ten families are hunting for a new home, but there are only five places up for grabs. What happens next is a bidding war. Prices climb until only those who can afford the premium are left standing. This exact scenario is playing out in major cities all over the world, turning the dream of an affordable home into a cutthroat competition.

This fundamental imbalance is the engine driving up costs for everyone, whether you're looking to rent or buy.

What's Causing the Shortage?

A perfect storm of factors has shrunk the housing pool. For years, we've seen sluggish construction rates, tangled up in restrictive zoning laws that make it a nightmare to build anything new. At the same time, people have been flocking to cities for better jobs and opportunities, causing demand in urban centers to explode.

The problem is, supply just can't keep up.

The gap between housing supply and demand has hit a breaking point. As of 2025, it's estimated there's a shortfall of 6.5 million housing units across key developed economies just to meet current needs. This scarcity has pushed homeownership out of reach for many, with over 80% of households in these markets now favoring renting because ownership is just too expensive. You can find more insights into this global living shift on Hines.com.

The bottom line is that scarcity is setting the price. From London to Los Angeles, the story is the same: limited inventory forces people to pay a premium for whatever they can get. This isn't just about market dynamics; it's a structural failure to build enough homes for a growing population, leaving millions priced out of the market.

How to Calculate What You Can Really Afford

Understanding the market is one thing, but knowing your own budget is where the real power lies. Before you even think about looking at listings, you need a crystal-clear picture of what you can realistically afford each month without stretching your finances to the breaking point. This means looking beyond your salary and getting honest about your total debt and monthly expenses.

There are a couple of foundational rules in personal finance that can really help guide you here. The first is the price to income ratio, which is a quick and dirty way to compare the median home price in an area to the median household income. It gives you a fast snapshot of local affordability.

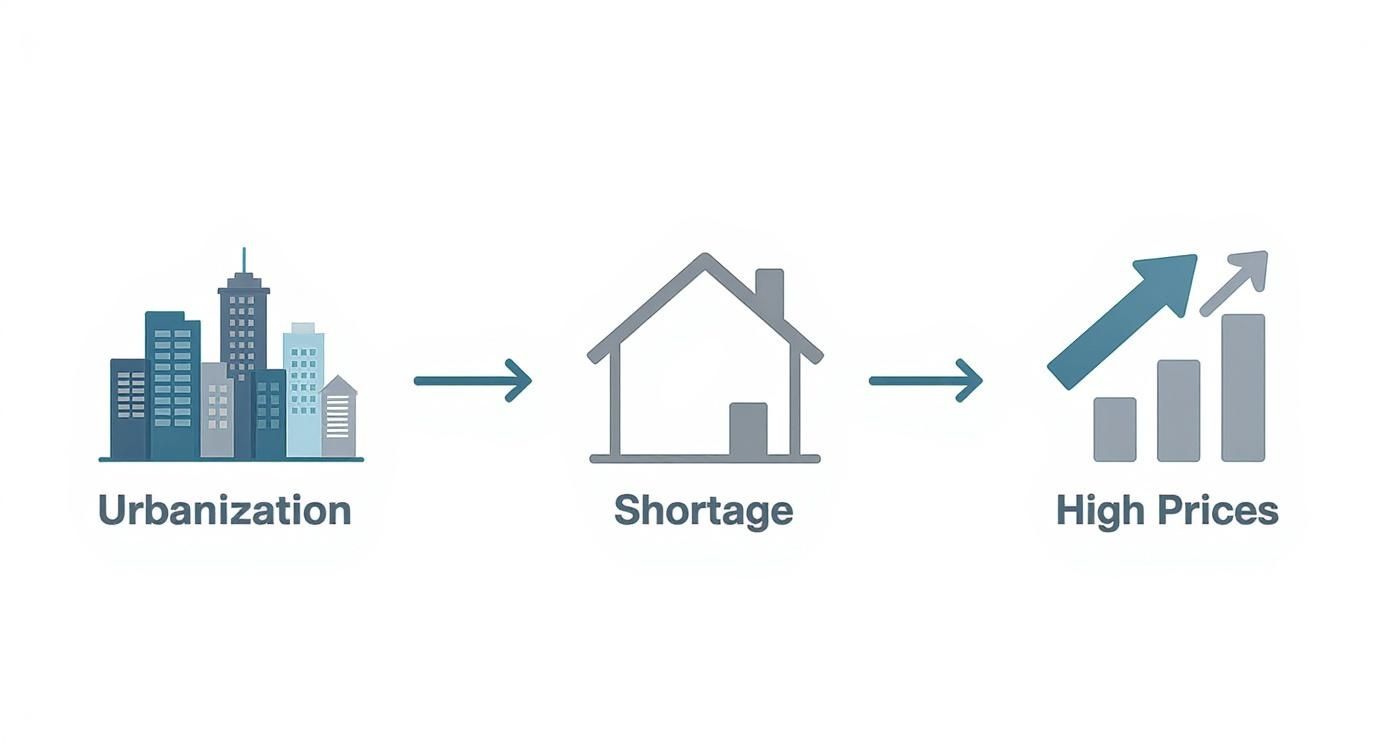

This infographic breaks down the chain reaction that leads to today's high housing costs.

As you can see, it often starts with increased urbanization, which creates housing shortages and, in turn, drives up prices. This isn't a new phenomenon; we've seen this trend play out globally for years.

In fact, housing affordability has gotten significantly worse over the last two decades. The 2025 Demographia International Housing Affordability report confirmed this, showing that the gap between home prices and household incomes continues to widen across 95 major markets. It's a trend that's putting immense pressure on middle and working-class families.

Applying the 28/36 Rule

For a more personal and practical guideline, turn to the 28/36 rule. This is a classic tool that lenders often use to figure out how much they're willing to lend you.

- The 28% Rule: Your total housing costs that’s your mortgage or rent, plus property taxes and insurance should not be more than 28% of your gross monthly income.

- The 36% Rule: Your total debt payments, which includes housing plus car loans, credit cards, and student loans, should not exceed 36% of your gross monthly income.

Let's make that real. If your household brings in $6,000 a month, your total housing costs shouldn't top $1,680 (28% of $6,000). On top of that, all your debt payments combined shouldn't go over $2,160 (36% of $6,000).

This rule provides a solid framework for figuring out what you can truly afford. It helps you separate your financial commitments to make sure you stay on stable ground. To get a better handle on this, check out our guide on understanding fixed and variable cost management.

A Closer Look at the US Housing Market

To really understand how global trends hit home, it helps to zoom in on a specific country. The United States housing market is a perfect example and it’s a fascinating paradox right now.

We're seeing an increase in new home construction, but the total number of homes actually for sale is still frustratingly low. This is the core dynamic keeping prices high, even when the pace of sales slows down.

The culprit? Sustained high interest rates have essentially put the market on ice. On one hand, potential buyers are getting squeezed by expensive mortgages, which naturally pushes demand down. On the other hand, homeowners who wisely locked in ultra-low rates a few years ago have no incentive to sell. Moving would mean trading their comfortable mortgage for a much higher one.

It's created a stalemate. With so few existing homes hitting the market, sales volume is sluggish, but the incredibly tight supply keeps prices from taking a nosedive.

Supply Constraints and Price Projections

This lack of existing homes for sale has created a solid floor under prices. A major market correction is unlikely unless we see some dramatic economic shifts.

Looking ahead to 2025, the consensus is that this slow-but-steady price growth will continue, all thanks to the high-rate environment and stubborn inventory problems. J.P. Morgan Research is forecasting a modest 3% increase in home prices for the year.

Even with the number of new homes for sale hitting 481,000 units the highest level we’ve seen since 2007 it’s not enough to fill the gap. The inventory of existing single-family homes is still 20-30% below previous lows. This shortage is what’s limiting options for buyers and keeping the cost of housing elevated.

When you’re staring down a high-cost housing market, it’s easy to feel overwhelmed. But getting paralyzed by sticker shock isn't the answer. Taking proactive, strategic steps can make all the difference between sitting on the sidelines and actually getting into a home. It’s time to move past just understanding the problem and start finding real solutions. This often means adjusting your expectations and exploring every possible angle to find a foothold.

Instead of getting hyper-focused on that traditional single-family home in a prime neighborhood, broadening your search can unlock a world of more affordable options. Sometimes, looking at alternative types of housing is the most accessible entry point into the market.

Expand Your Housing Search

Being flexible with the type of property and its location can dramatically increase your options and bring prices back down to earth.

- Explore Condos and Townhouses: These attached homes almost always come with a lower price tag than a standalone house in the same area. They're a fantastic way to start building equity without the massive initial investment.

- Look at Emerging Suburbs: With remote work becoming a permanent fixture for many, once-overlooked suburbs are getting a second look. These areas often deliver more space for your money and a lower cost of living, making them a smart alternative to pricey urban centers.

Strengthen Your Financial Position

Your personal finances are the bedrock of any home purchase. Getting your financial house in order doesn't just increase your budget; it makes you a much more attractive borrower in the eyes of lenders, opening the door to better loan terms and lower interest rates. In a competitive market, a strong financial profile is your best weapon.

A disciplined approach to saving and credit management can dramatically lower the long-term cost of owning a home.

A higher credit score can be the difference between a good mortgage rate and a great one. Even a small reduction in your interest rate can save you tens of thousands of dollars over the life of your loan. This is where financial discipline pays direct dividends.

Don't forget to look into government and non-profit programs designed to help buyers clear financial hurdles. A quick search for down payment assistance programs in your state or city could uncover the boost you need to close the deal. For those juggling complex budgets, applying principles from the tech world like those used in cloud cost optimisation can reveal surprising ways to save. By systematically tracking where your money goes and cutting back, you can supercharge your savings and get closer to your housing goals faster than you thought.

Questions We Often Hear About Unit Costs

When you're trying to make sense of today's high housing costs, a lot of questions pop up. Let's tackle some of the most common ones with straightforward answers to clear up the confusion.

What Is the Single Biggest Factor Driving Costs?

At its core, the problem is a classic case of supply and demand being way out of balance. In nearly every major market, there are far more people looking for a home than there are homes available. That scarcity is the number one reason prices have shot up.

Think about it: when you have limited new construction, zoning laws that make it hard to build, and more people moving into cities, you create a pressure cooker environment. This dynamic makes every existing unit incredibly valuable and, unfortunately, much less affordable for the average person.

Will Housing Unit Costs Go Down Soon?

It’s unlikely we'll see a big drop anytime soon. Most experts are forecasting that price growth will slow down, but not reverse. The simple reason is that the chronic shortage of homes for sale acts as a floor, preventing prices from tumbling.

Even with higher interest rates cooling off some buyer enthusiasm, the lack of inventory means the few homes that are available still attract plenty of competition. For prices to fall sharply, we'd probably need a major economic downturn or a massive, sustained building boom and neither seems to be on the horizon. The principles here aren't too different from what drives infrastructure expenses, which we explore in our guide on the true cost of cloud.

A common misconception is that falling demand will automatically lead to cheaper housing. However, without enough homes for sale, prices remain stubborn because the few available units still attract competitive offers.

How Can I Find More Affordable Housing Options?

Finding a place you can afford today demands a bit of creativity and a lot of research. The best first step is to broaden your horizons look at smaller cities or suburban areas just outside the major hubs where prices are often significantly lower.

You should also explore different types of homes. Condos and townhomes, for example, can be a more accessible entry point into the market than a traditional single-family house. Don't forget to look into federal, state, and local homebuyer assistance programs; they can provide critical help with down payments or closing costs, making a huge difference in your long-term cost of units.

Ready to cut costs in other areas of your business? CLOUD TOGGLE helps organizations reduce cloud spend by automatically powering off idle servers. Start your 30-day free trial and see how much you can save at https://cloudtoggle.com.