Cost allocation is really just the process of splitting up shared business expenses and assigning them to different departments, projects, or products. Think of it like an itemized receipt for your company's internal spending. Instead of one big, mysterious number for overhead, you get a clear breakdown of who used what.

This simple act of divvying up costs is fundamental to understanding your business's true profitability and making smarter financial decisions.

Why Does Accurate Cost Allocation Matter So Much?

Imagine trying to figure out if your hot new product is actually a success without knowing how much it really cost to make. Sure, the sales numbers look great, but what about its share of the factory rent, the marketing team's salaries, or the IT support it required? Those hidden expenses could be silently eating away all your profits.

This is the exact problem that good cost allocation solves. It’s not just some boring accounting task; it’s a strategic tool that brings financial clarity to your entire operation. Without it, you're flying blind, making big decisions with incomplete or, worse, misleading information.

Getting to True Profitability

The biggest win from clear cost allocation is discovering the real profitability of every piece of your business. A product that looks like a winner on paper might actually be a financial black hole once you assign its fair share of overhead.

On the flip side, another product might be a quiet superstar, generating far more value than you realized. This kind of detailed insight helps you:

- Spot Your Winners: Pinpoint which products, services, or departments are creating the most value.

- Find the Hidden Leaks: Recognize which initiatives are draining more resources than they're worth.

- Nail Your Pricing: Set prices that truly reflect the total cost of getting a product or service to a customer.

When you know your true cost structure, you can confidently double down on what works and cut or fix what doesn’t. It’s the only way to steer the ship toward sustainable growth.

Driving Accountability and Efficiency

When departments see a bill for the resources they actually use, they start spending more mindfully. It's human nature. This simple change builds a culture of accountability where team leaders think twice about their operational costs.

This is especially true for shared services like IT, HR, and facilities. For many large companies, 30–50% of all costs are allocated from these shared services, so getting the distribution right is critical for keeping the peace and showing where the money is really going. As a detailed report from Deloitte points out, unclear rules often lead to arguments over fairness and hide the real cost drivers.

Ultimately, effective cost allocation turns abstract overhead into real numbers that people can act on. It lays the groundwork for a financially transparent company where every team understands its impact on the bottom line and is motivated to improve it.

Exploring Core Cost Allocation Methods

Choosing a cost allocation method can feel like picking a tool from a toolbox. You wouldn't use a sledgehammer for a small nail, and the same logic applies here. The right method depends entirely on the job you need it to do, from getting a quick, directional sense of costs to achieving pinpoint accuracy.

To get started, it's helpful to understand the foundational approaches that most companies build on. Each one strikes a different balance between simplicity and precision, making them a good fit for different types of organizations and goals. Let's break down three of the most common ones.

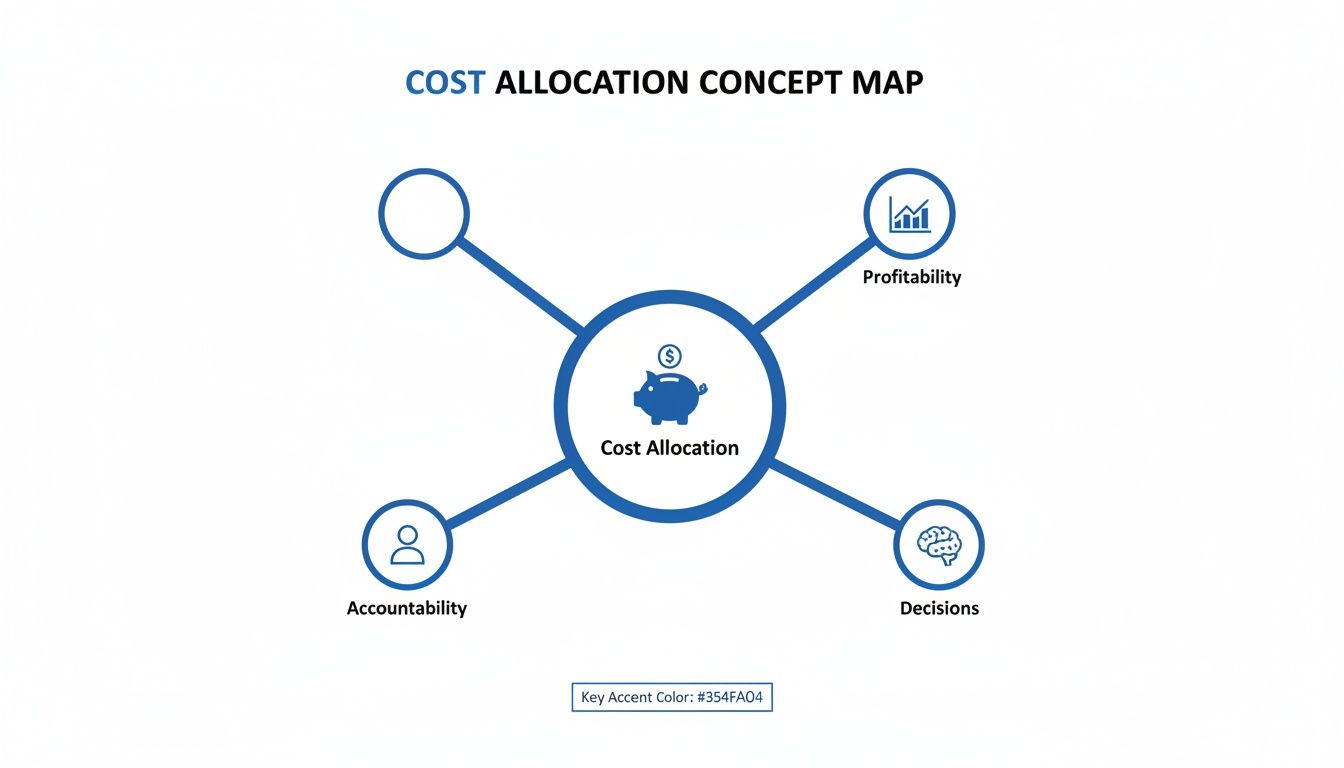

This concept map shows how cost allocation is the linchpin for profitability, smart decision-making, and clear accountability.

Ultimately, a solid allocation strategy isn't just an accounting exercise; it's a core business function that drives real results.

The Direct Method

The Direct Method is as straightforward as it gets. It takes the total costs from a support department, like IT or HR, and assigns them directly to the primary business units that use their services. Simple.

Crucially, it completely ignores any services that support departments provide to each other.

Imagine an IT team that supports a marketing department and a sales department. If the marketing team is responsible for 70% of the IT help desk tickets and sales is responsible for 30%, the IT department’s entire budget gets split right down that line. It's clean, simple, and incredibly easy to calculate.

- Best For: Younger or smaller companies where support departments have very little interaction with each other. It's perfect for startups that just need a "good enough" answer without getting bogged down in complexity.

- Potential Blind Spot: Its greatest weakness is its lack of precision. If the IT department also spends a lot of time supporting the HR team, the Direct Method overlooks that entirely. This can easily distort the true cost of running each part of the business.

The Step-Down Method

The Step-Down Method (also called the sequential method) adds a much-needed layer of sophistication. It acknowledges the reality that support departments don't just help the revenue-generating teams, they help each other, too.

This method allocates costs in a sequence. You start with the support department that provides the most services to other support departments and distribute its costs first. Once a department's costs are allocated out, it's "closed," and no further costs are assigned back to it.

For example, if HR serves every other team, its costs are spread across IT, marketing, and sales first. Then, the IT department's new total cost (its original budget plus the share from HR) is allocated to just marketing and sales. It's a one-way street for costs.

This one-way flow of costs provides a much more accurate picture than the Direct Method without becoming overly complicated. It’s a practical middle ground for growing businesses.

This approach gives you a better reflection of how resources are actually consumed inside a more interconnected organization.

Tag-Based Allocation

In the world of cloud computing, Tag-Based Allocation has become the undisputed gold standard. Cloud resources like servers, databases, and storage are spun up and down so quickly that traditional monthly allocation methods just can't keep up.

Tagging is all about applying metadata labels (the tags) to every single cloud resource. These tags can identify a resource's owner, project, cost center, or environment (like "production" or "development").

When the monthly bill from AWS or Azure arrives, the costs are automatically sorted and assigned based on those tags. Any resource tagged with project:phoenix is instantly allocated to the Phoenix project's budget. No guesswork needed.

This method gives you an incredibly granular and accurate view of spending, which is absolutely essential for managing sprawling cloud environments. It transforms cost allocation from a painful monthly accounting exercise into a real-time, automated process.

Comparison of Foundational Cost Allocation Methods

To help you figure out which approach might fit your organization's needs, here’s a quick side-by-side look at these three foundational methods.

| Method | Core Principle | Best For | Complexity Level | Accuracy |

|---|---|---|---|---|

| Direct Method | Assigns support costs only to operating departments. | Simple organizational structures with minimal cross-team support. | Low | Low to Moderate |

| Step-Down Method | Allocates support costs sequentially in a one-way flow to all teams. | Organizations with some inter-support department services. | Moderate | Moderate to High |

| Tag-Based Allocation | Assigns costs based on metadata tags applied to individual resources. | Cloud-native companies and dynamic, complex IT environments. | High (to set up) | Very High |

Getting a handle on these methods gives you a solid foundation. While simpler approaches work for some, businesses with high overhead or complex operations usually need to layer on more advanced strategies to truly understand the cost of doing business.

How Activity-Based Costing Reveals What Things Really Cost

Simpler cost allocation methods are a decent starting point, but they often paint a blurry picture, especially when your overhead is high. This is where Activity-Based Costing (ABC) comes in to offer a much sharper, more accurate financial lens.

Instead of smearing costs across the board using broad averages like labor hours, ABC gets granular. It digs in to connect costs directly to the specific activities that actually create them.

Think of it this way: a simple allocation method is like splitting a dinner bill evenly among friends, no matter who ordered the pricey steak and lobster. ABC is the itemized receipt that shows exactly who ordered what, making sure everyone pays their fair share. This level of detail can completely change how you see your operational costs and which products are truly profitable.

The whole idea behind ABC is to pinpoint key business activities, group the costs for those activities into "cost pools," and then assign those costs to products or services based on how much they actually use each activity.

The ABC Framework in Action

Putting ABC into practice is definitely more involved than the simpler methods, but the clarity you get is almost always worth the effort. The process breaks down into a few logical steps:

- Identify Activities: First, you map out the major activities that drive costs in your organization. This could be anything from machine setups and quality inspections to customer service calls or processing purchase orders.

- Assign Costs to Activities: Next, you add up all the overhead costs tied to each of those activities. For example, the "machine setup" cost pool would include the salaries of the technicians involved, the cost of their tools, and any related supplies.

- Identify Cost Drivers: For each activity, you need to figure out its "cost driver," the unit of measure for that activity. For machine setups, the driver is simply the number of setups. For quality control, it might be the number of inspections.

- Allocate Costs: Finally, you divide up the costs from each activity pool and assign them to your products based on how many units of the cost driver they consumed.

This granular approach gives you a far more precise and honest distribution of your overhead.

Uncovering Hidden Truths with an Example

Let's imagine a factory making two products: a high-volume, simple Product A and a low-volume, complex Product B. The factory has a hefty $100,000 in maintenance overhead, mostly driven by the time and effort of setting up the machines.

- Product A: Requires only 5 machine setups to churn out 10,000 units.

- Product B: Needs 95 machine setups to produce just 1,000 units because of its complexity.

A traditional method might just allocate that maintenance cost based on production volume, which would be completely misleading. But with ABC, we allocate based on the real activity driver: the number of setups.

By linking costs to the activities that cause them, ABC reveals that low-volume, complex products can be far more expensive to produce than they initially appear. This is the kind of critical insight that traditional cost allocation methods almost always miss.

Using this more accurate model, Product B would be assigned 95% of the maintenance overhead ($95,000), correctly showing how much it really demanded from the setup team. This might suddenly reveal that Product B, which you thought was a winner, is actually losing money. Making decisions with this kind of clarity is a huge strategic advantage.

To see more ways this plays out, you can learn more about Activity-Based Costing in our other articles.

Activity-Based Costing really took off as a direct response to the glaring inaccuracies of older, volume-based systems. As automation ramped up in manufacturing, overhead costs ballooned, sometimes making up 40–50% of total costs and rendering those simple allocation methods dangerously unreliable.

Implementing Cost Allocation in the Cloud

Trying to apply old-school cost allocation methods to the cloud is like using a city map to navigate the open ocean. The landscape is dynamic, resources spin up and down in minutes, and costs can balloon without warning. To get a handle on it, you need a strategy built for this fluid world, and that's where FinOps principles and cloud-native techniques come in.

Managing cloud spend isn't a once-a-quarter accounting exercise anymore. It's about real-time financial governance. Two key FinOps ideas that help build this culture are Showback and Chargeback.

- Showback: This is simply tracking and reporting cloud costs back to the teams or departments that incurred them. No money changes hands; the goal is pure visibility. It’s a gentle way to introduce accountability by showing teams the financial impact of their work.

- Chargeback: This takes it a step further by actually billing departments for their cloud usage. It creates direct financial responsibility and gives teams a powerful reason to optimize their resources and control their spending.

This image shows how distinct tags like Cost Center, Project, and Environment are used to categorize resources, which is the first step toward effective financial tracking and reporting.

Mastering Tag-Based Allocation

The foundation of any solid cloud cost strategy is a robust tagging policy. Think of tags as simple key-value metadata labels you attach to every cloud resource, a server, a database, a storage bucket. Done right, they let you slice and dice your cloud bill with incredible precision.

But a sloppy tagging strategy leads to a mess of "untaggable" or uncategorized costs, which can easily eat up a huge chunk of your bill. Nailing down a solid policy from day one is non-negotiable.

Your policy needs to define a set of mandatory tags for all new resources. Common ones include:

cost-center: Which business unit pays for this?project: What initiative is this resource tied to?owner: Who is the person or team responsible?environment: Is this forprod,dev, orstaging?

The goal is simple: make sure every dollar of cloud spend can be tied back to a specific business purpose. Without comprehensive tagging, you’re just staring at a massive, confusing bill that’s impossible to allocate fairly.

Handling Shared Costs and Commitments

Of course, not everything fits neatly into a tag. What about shared services like networking infrastructure, monitoring tools, or a central data platform that everyone uses? These shared costs have to be split proportionally based on usage. For instance, you could divide the cost of a shared database based on the volume of API calls each application makes.

Then there’s amortization. When you make big upfront commitments like buying AWS Reserved Instances or Savings Plans, you pay for capacity in advance to lock in a discount. Amortization is the accounting practice of spreading that one-time cost over the entire commitment term (usually one or three years). This avoids a massive cost spike in a single month and gives you a much truer picture of your ongoing operational expenses. To do this right, you need detailed data from tools like the AWS Cost and Usage Reports.

Automating for Scale and Accuracy

Let's be realistic: manually enforcing a tagging policy across a sprawling cloud environment is a losing battle. Automation is the only way to keep your data accurate and scale your efforts.

You can use policy-as-code tools like AWS Service Control Policies or Azure Policy to automatically block the creation of untagged resources. You can also run scripts that periodically scan for non-compliant resources, either flagging them for someone to fix or tagging them automatically based on predefined rules. This keeps your cost data clean and reliable, turning cloud cost allocation from a painful, reactive chore into a proactive, automated system that drives financial discipline.

How to Choose the Right Allocation Method

Moving from theory to practice means picking a cost allocation method that actually fits your business. There’s no single “best” answer; the right choice always depends on real-world factors like your company's size, the complexity of your operations, and the level of precision you genuinely need.

It's all about finding the sweet spot between effort and insight.

A small startup, for instance, might be perfectly happy with the direct method. It gives them a quick, directional view of costs without bogging down a lean team. On the other hand, a huge enterprise with multiple service departments and intricate product lines will almost certainly need a hybrid approach. They might blend Activity-Based Costing (ABC) for manufacturing overhead with tag-based allocation for their cloud infrastructure.

Balancing Accuracy with Effort

The key to a winning strategy is understanding a simple accounting principle: materiality.

It boils down to one question: will the extra effort of a more complex method give you insights valuable enough to justify the work? Implementing a full-blown ABC system is a heavy lift, but for a manufacturer, it could be a game-changer. Imagine discovering your flagship product is actually unprofitable, that’s the kind of insight that justifies the investment.

You have to weigh the cost of implementation against the value of the information you get back. Sometimes, "good enough" is truly the best financial decision. It’s about being pragmatic and focusing your analytical firepower where it will have the biggest impact on your bottom line. An effective cost allocation strategy is a core part of any healthy FinOps practice. To learn more about this framework, check out our comprehensive guide on what is FinOps.

How Business Models Shape Your Choice

Different business models naturally pull you toward different allocation strategies. Let's look at a couple of contrasting examples to see how this plays out in the real world.

Case Study 1: A Manufacturing Firm

A company that makes physical goods has massive overhead tied up in its factory, machinery, and support staff.

- Primary Challenge: How do you accurately assign costs like factory rent, equipment depreciation, and quality control salaries to a diverse product line?

- Best Fit: Activity-Based Costing is often perfect here. Allocating costs based on specific drivers, like machine setup hours or the number of inspections, paints a far more accurate picture than just spreading costs based on something generic like labor hours.

Case Study 2: A SaaS Company

A software-as-a-service provider operates almost entirely in the cloud. Its main costs are engineering salaries and cloud infrastructure spend.

- Primary Challenge: How do you attribute dynamic, fluctuating cloud spend to specific features, customers, or development teams?

- Best Fit: Tag-based allocation is non-negotiable. When you combine it with a showback or chargeback model, you create direct accountability for the engineering teams consuming those resources. Any shared platform costs can then be allocated proportionally based on metrics like API call volume.

The choice of allocation method isn't just an accounting decision; it's a strategic one that directly impacts how you perceive and manage your business's financial health.

The method you choose can seriously change the final numbers. For instance, public economics research shows that different allocation rules can swing a party's assigned cost share by 20–100%. In airport cost studies, just switching the cost driver from passenger throughput to gate hours has shifted an airline's rate burdens by as much as 15–50%. This proves just how much the underlying logic matters. You can explore more about these distributional effects in infrastructure cost allocation research.

Of course. Here is the rewritten section, crafted to sound like it was written by a human expert and matching the requested style and formatting.

Common Questions About Cost Allocation

Even with the best strategy in hand, cost allocation can get tricky. Let's tackle some of the most common questions that pop up, so you can move forward with confidence. Getting these details right is the difference between a financial system that works and one that just creates confusion.

What Is the Difference Between Cost Allocation and Cost Apportionment?

You’ll often hear these two terms used interchangeably, but they’re actually two different tools for assigning costs. It’s a subtle but important distinction.

Cost allocation is simple and direct. It's when you can assign an entire cost to a single department or team. Think of a department manager's salary, it’s a direct cost, so you allocate 100% of it to their specific department. Easy.

Cost apportionment, on the other hand, is for shared costs. This is when you have to split an indirect cost across multiple parts of the business in a fair way. A perfect example is the rent for your office building; you might apportion it to different departments based on the square footage each one uses.

In short, you allocate costs you can directly trace, and you apportion costs you have to fairly share.

Nailing this difference is a foundational step to building a cost model that actually makes sense.

How Often Should a Business Review Its Cost Allocation Methods?

Your cost allocation model is not a "set it and forget it" tool. You should be reviewing it at least annually, or whenever your business goes through a major change. Using an outdated model is a recipe for bad data and, ultimately, poor decisions.

You should plan an immediate review if any of these things happen:

- A Major Restructuring: If you reorganize teams, departments, or entire business units, your old allocation logic is probably obsolete.

- A Big Operational Shift: Moving a significant workload to the cloud, launching a new product line, or heavily investing in automation all change your cost structure and demand a review.

- The Numbers Just Feel Wrong: If managers are constantly questioning their allocated costs or the data no longer reflects reality, it’s a huge red flag. Your drivers or methods aren't working anymore.

Regular check-ins keep your financial data relevant and make sure it remains a reliable source for making smart business moves.

What Are the Biggest Challenges in Implementing Activity-Based Costing?

Activity-Based Costing (ABC) can give you incredible accuracy, but it’s not a walk in the park. Anyone considering it needs to be ready for a few significant hurdles.

The biggest challenges are its complexity and the sheer amount of resources it eats up. First off, you have to identify every single activity that drives costs in your organization. This is a massive undertaking that requires a deep understanding of your operations, from the ground up.

Next comes the data problem. You have to gather data for all your new activity drivers, and your current systems might not be set up to track things like the number of machine setups, customer support calls per product, or quality inspections performed. Getting that data can be a project in itself.

Finally, you need buy-in from everyone. ABC isn't just a finance project; it requires cooperation from nearly every department. The initial setup and ongoing maintenance are expensive, which is why it's usually a better fit for larger, more complex businesses where that level of precision is worth the hefty investment.

Can I Use Multiple Cost Allocation Methods at the Same Time?

Yes, absolutely. In fact, you probably should. A hybrid approach that mixes several cost allocation methods is not only common, it's a best practice for most companies.

A blended strategy lets you use the right tool for the right job, balancing accuracy with simplicity. For example, a business might use:

- The direct method for easy-to-track costs like salaries.

- A step-down method to allocate costs from internal support teams like IT and HR.

- Activity-based costing only for complex manufacturing overhead where you need extreme precision.

- Tag-based allocation for all cloud resources to get that crucial, granular visibility.

This practical approach keeps you from overcomplicating the simple stuff while still using more powerful methods where they’ll have the biggest impact. It’s all about building a system that is both accurate and manageable.

Ready to stop wasting money on idle cloud resources? CLOUD TOGGLE makes it easy to automate server schedules, reduce your cloud bill, and build a culture of cost accountability without complex setups. Start your free 30-day trial and see how much you can save at https://cloudtoggle.com.